Keywords: workers’ compensation injuries, WC coverage, work-related injury claims, workers’ comp 2025, workplace injury coverage, NCCI workers comp, denied claims workers comp.

Introduction: Understanding Workers’ Compensation Coverage

Workers’ compensation is something every employer and employee hears about, but most people misunderstand what’s truly covered. Some assume, “if it hurts, it’s covered,” but that’s not always correct. Workers’ comp 2025 rules can be head-spinning; state laws vary, and insurers interpret coverage differently.

Generally, workers’ compensation covers medical expenses and lost wages when injuries are directly tied to work—but not every situation qualifies. Some claims are denied, some are partially paid, and some are only covered if proper documentation exists. Understanding what’s covered—and what isn’t—can save headaches and delays.

1) Injuries Normally Covered by Workers’ Compensation

a) Acute Physical Injuries

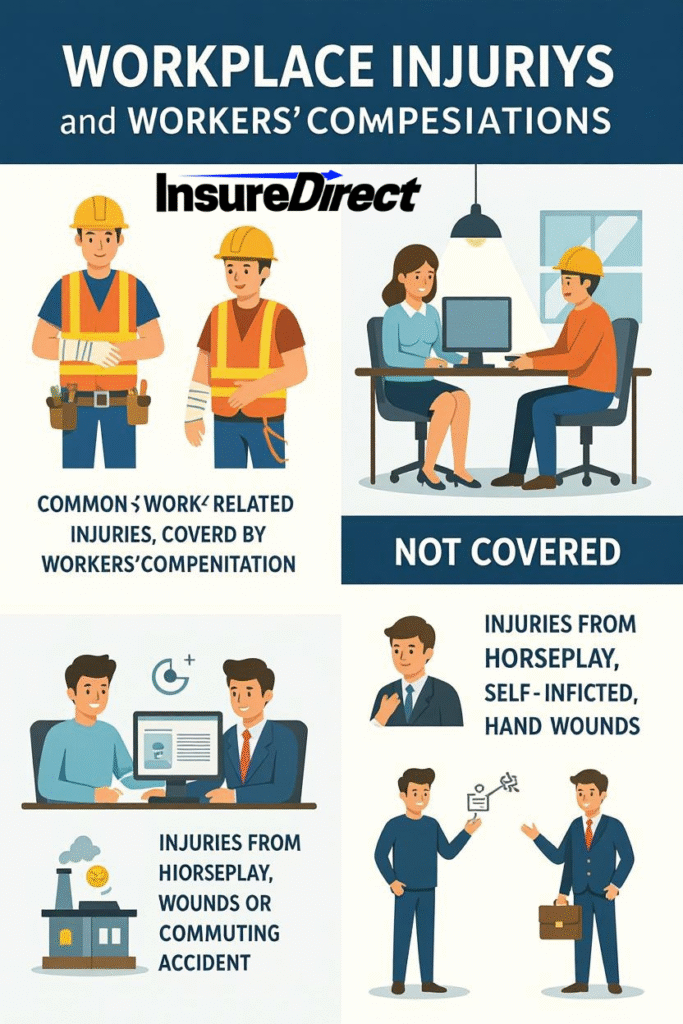

The most common workers’ comp claims are from sudden accidents, including slips, falls, machinery incidents, or being struck by objects. Examples:

- Fractured bones

- Sprains and strains

- Cuts requiring stitches

- Burns

In most states, these injuries are presumed work-related if they occur at the workplace. Timely reporting is crucial; failure to report immediately can delay or deny benefits.

b) Repetitive Stress Injuries

Some injuries develop gradually. Repetitive stress injuries—like carpal tunnel syndrome, tendonitis, or rotator cuff strain—may be covered if work activities caused or aggravated them.

Proving causation can be challenging. Employers might argue the injury stems from personal activities, such as sports. Medical evaluations and ergonomic assessments often determine if the injury is compensable.

c) Occupational Diseases

Employees can develop illnesses from workplace exposure. Workers’ comp often covers:

- Respiratory illnesses from chemical exposure

- Skin conditions from prolonged irritants

- Noise-induced hearing loss

Coverage depends on showing that the disease is directly work-related and meets OSHA or state regulatory exposure thresholds.

d) Psychological or Mental Health Conditions (Occasionally)

Mental health claims were historically complex to cover. Modern workers’ comp now sometimes includes stress-related disorders, such as PTSD or anxiety caused by workplace trauma.

- First responders, police, and nurses exposed to traumatic events may qualify

- Documentation from therapists or physicians is generally required

- Coverage varies by state

2) Injuries Typically Not Paid by Workers’ Compensation

a) Injuries That Happen Off-the-Job

Injuries that occur outside work, like skiing on the weekend, are generally not covered. Exceptions include:

- Traveling for work

- Participating in employer-sanctioned events

Otherwise, off-the-job accidents are excluded.

b) Injuries Due to Employee Misconduct or Intoxication

Workers’ comp usually excludes injuries caused by:

- Illegal activity

- Intoxication at work

- Fighting or reckless behavior

Examples:

- Breaking a hand in a bar fight during lunch

- Slipping while intoxicated at work

- Misusing machinery against company rules

Claims under these circumstances may be denied.

c) Pre-existing Conditions Not Aggravated by Work

Old injuries are only covered if work materially worsened the condition.

Example: mild knee arthritis aggravated by concrete floors at work may be partially covered. If unrelated to job duties, the claim is denied.

d) Normal Wear-and-Tear or Self-Inflicted Injuries

Workers’ comp generally does not cover age-related wear and tear or self-inflicted injuries. Medical evidence and independent evaluations usually determine claim eligibility.

3) Special Situations

a) Travel and Commuting Injuries

Most states exclude normal commuting injuries from coverage. Exceptions:

- Business travel or client visits

- Traveling between work locations while on call

Slipping in the parking lot on the way to work usually isn’t covered.

b) Workplace Violence

Injuries from assaults at work can be covered if directly related to employment:

- A customer attacked retail workers

- Security personnel were harmed on duty

c) Telecommuting and Remote Work Injuries

Remote work has complicated coverage. Home-office injuries may qualify if:

- Injury occurs while performing work tasks

- The home office is documented as a workspace

- Employer has established remote-work policies

4) Denied Workers’ Compensation Claims — Why They Happen

Even valid injuries can be denied for reasons such as:

- Delayed reporting of the injury

- Insufficient medical documentation

- Disputes over causation

- Alleged policy violations

Employees often engage workers’ comp attorneys to appeal denied claims. Administrative hearings can overturn initial insurer decisions.

5) Steps to Ensure Your Injury is Covered

- Report injuries immediately to your supervisor or HR

- Seek medical treatment promptly; use authorized providers if required

- Document accidents thoroughly, including witnesses, photos, and pre-existing conditions

- Follow recommended therapy and treatments

- Understand your state’s workers’ comp regulations

6) Workers’ Compensation Benefits

Covered claims can provide:

- Medical treatment for injuries

- Wage replacement for lost time (temporary or permanent)

- Rehabilitation or retraining if unable to return to previous work

- Death benefits for survivors

State laws set benefit limits and pre-approval requirements.

7) How Employers Can Minimize Denials

Employers can assist by:

- Establishing clear reporting procedures

- Training managers to identify injuries early

- Keeping accurate injury records

- Encouraging use of approved providers

- Reviewing WC policies annually

These steps help reduce disputes, ensure timely treatment, and maintain stable premiums.

8) Common Myths

- “If it hurts at work, it’s automatically covered” — False

- “Workers comp covers every injury” — False; pre-existing, off-the-job, and misconduct injuries usually excluded

- “Mental health claims aren’t covered” — Partially true; PTSD and stress-related claims are sometimes covered

- “Commuting injuries count” — False, except in specific work-related travel

9) Emerging Trends in Workers Comp 2025

- Remote work injury claims are rising

- Mental health coverage is expanding, especially for first responders

- Off-site ergonomic injuries are gaining attention

- Insurers increasingly use fraud detection tools

These trends are significant for employers and employees to anticipate future claims and coverage issues.

10) SEO-Friendly Closing Paragraph (Meta + CTA)

Workers’ compensation protects both employees and employers from financial losses caused by workplace injuries. Knowing what is and isn’t covered ensures faster claims, fewer disputes, and better recovery outcomes.

Employers should provide clear guidelines, maintain compliance with WC laws, and track workplace accidents. Employees should report injuries promptly, document thoroughly, and consult medical professionals for all work-related incidents.

Want to understand how your 2025 workers’ comp coverage applies? Check state-specific rules or have a workers’ compensation attorney or broker review your coverage today.

Sources & References

- NCCI — Workers Compensation Coverage Basics

- OSHA — Work-Related Injuries and Illnesses

- WCRI — 2025 Workers Compensation Trends

- Enlyte — Workers Comp Injury Reports

- Federal Register — Remote Work Injury Coverage Rules

InsureDirect.com

Corporate Home Office

618 South Broad Street

Lansdale, Pennsylvania 19446

Email: contact@insuredirect.com

Phone: (800) 807-0762 ext. 602Keep your home safe and secure with complete protection from InsureDirect—because your home deserves nothing less than the best.