Workers’ compensation insurance is often misunderstood. Many employers think they “know it all,” yet myths persist. It’s a safety net, yes, but how it works, who it covers, and how much it costs—misconceptions are everywhere. In this article, we’ll bust common workers’ compensation insurance myths, clarify facts, and explain why businesses and employees need coverage.

What Is Workers’ Compensation Insurance?

Workers’ compensation insurance, or “workers comp,” provides benefits to employees who are injured at work or develop job-related illnesses. It helps cover medical bills, lost wages, and rehabilitation costs in some cases.

{kind=link}

Some think it’s unnecessary, while others believe it’s only for big companies. Neither is true. Even small businesses with a single employee are generally legally required to carry coverage.

Key Point: Workers comp insurance isn’t “nice to have”—it’s a legal mandate in most U.S. states.

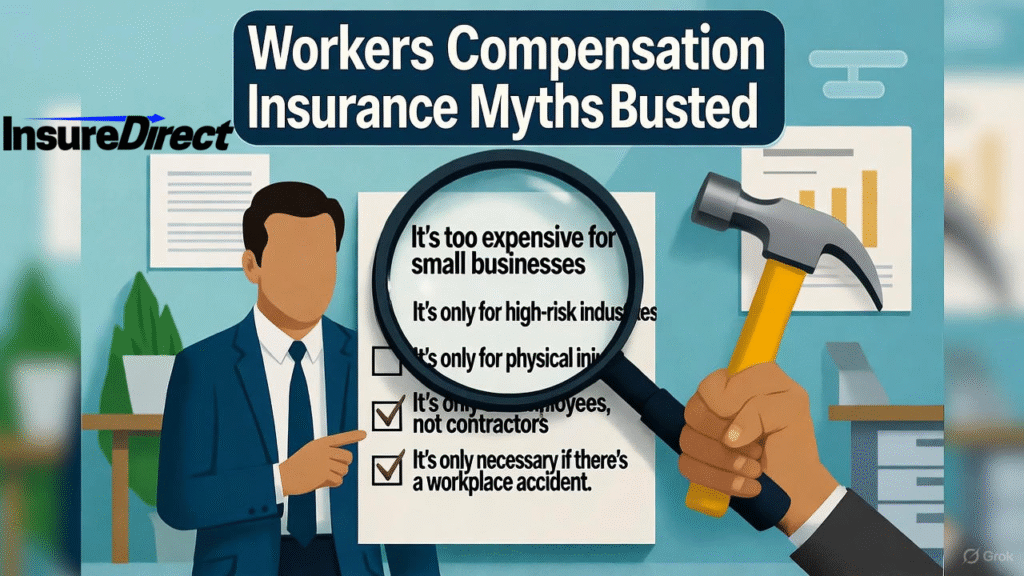

Common Misconceptions About Workers’ Compensation Insurance

Despite its importance, myths about workers’ comp abound. Let’s debunk the most common ones.

Myth 1: “Workers’ Compensation Is Only For Hazardous Jobs”

Some employers assume only factory workers, construction employees, or miners need coverage. That’s false! Every workplace—from offices to retail stores—carries risk. Slips, trips, repetitive strain injuries, or stress-related illnesses can occur anywhere.

Fact: Office workers can also file claims. Repetitive strain injuries or office falls are valid.

Interestingly, a 2019 study found that over 20% of claims originated from office settings—not what most people expect.

Myth 2: “Employees Can Sue If They Get Hurt”

Many believe workers’ comp prevents employees from suing employers. Partially true. Workers’ comp usually provides an exclusive remedy, meaning most employees cannot sue for negligence. But exceptions exist: gross negligence, intentional harm, or lack of insurance can allow lawsuits.

Fact: Workers’ compensation reduces lawsuits but does not eliminate them entirely.

Myth 3: “Workers’ Compensation Covers Everything”

Some think workers’ comp covers literally everything related to a workplace injury. Not so. Items often not covered include:

- Pain and suffering (usually)

- Injuries unrelated to work

- Some long-term disabilities outside work

Fact: Employers and employees must understand what workers’ compensation actually covers.

Myth 4: “It’s Too Expensive, So We Don’t Need It”

Small business owners often fear premiums. Insurance rates depend on company size, industry, and claims history. Many policies are surprisingly affordable, even for small firms. Paying up front is usually cheaper than lawsuits, fines, or uncovered medical expenses.

Fact: Cost should never prevent legally required coverage.

Myth 5: “Only Full-Time Employees Are Covered”

Some think part-time, temporary, or contract workers aren’t eligible. Coverage depends on state laws and employment classification. Most part-time workers are included, but independent contractors usually are not. Misclassifying employees can result in penalties.

Fact: Misunderstanding coverage eligibility is a common and expensive mistake.

Why Workers’ Compensation Insurance Is Essential

Even after debunking myths, some employers remain hesitant. Here’s why coverage is crucial:

- Protects Employees Financially: Covers medical bills, lost wages, and rehabilitation.

- Protects Employers Legally: Reduces lawsuits and liability risks.

- Promotes Workplace Safety: Companies with coverage often implement safety programs.

- Ensures Legal Compliance: Coverage required in nearly all states.

How Premiums Are Calculated

Confusion about premiums contributes to misconceptions. Factors include:

- Industry Risk: High-risk industries like construction pay more.

- Payroll Size: Higher payroll = higher premiums.

- Claims Experience: Fewer claims = lower premiums.

- State Requirements: Each state defines minimum coverage and rules.

Fact: Understanding how workers’ compensation premiums are calculated helps employers budget effectively.

Real-Life Scenarios Illustrating Misconceptions

Scenario 1: Office Slip and Fall

An employee spills coffee and breaks a wrist. The employer assumes office injuries aren’t serious, but medical costs and lost wages are covered under workers’ comp.

Scenario 2: Employee With Chronic Condition

An employee with diabetes experiences an on-the-job flare-up requiring hospitalization. Employers often think pre-existing conditions void coverage. Wrong! Workers’ comp covers work-related injuries even with pre-existing conditions.

Scenario 3: Small Business Owner Avoiding Insurance

A shop owner skips coverage to save money. One accident, massive medical bills, and attorney fees exceed insurance costs several times over. Lesson: Skipping coverage is risky.

Misconceptions About Filing Claims

Both employees and employers often misunderstand claims processes:

- Myth: Filing a claim is slow and complicated.

-

- Fact: Modern systems and insurers streamline the process; many claims are handled quickly.

- Myth: You will be fired for filing a claim.

-

- Fact: Retaliation is illegal; employees are protected.

- Myth: Minor injuries aren’t covered.

-

- Fact: Even small injuries can have cumulative effects; claims are valid.

Workers’ Compensation and Digital Trends

Technology is transforming workers’ compensation:

- Online Claims: Employees can submit claims digitally.

- Telemedicine: Remote medical consultations are covered in some cases.

- Safety Monitoring: IoT devices track workplace hazards, reducing claims.

Fact: Employers adopting digital solutions often experience lower premiums and fewer claims.

SEO Keywords Naturally Integrated

- Workers’ compensation insurance myths

- What is workers’ compensation?

- Workers comp myths

- Affordable workers’ compensation insurance

- Small business workers’ comp

- Workplace injury insurance coverage

- Employee injury insurance

Tips for Employers to Avoid Misconceptions

- Educate Employees: Provide accurate information about coverage and claims.

- Hire Experts: Brokers and insurance agents help navigate policies.

- Review Policies Annually: Ensure coverage matches business needs.

- Promote Safety: Workplace safety programs reduce claims and premiums.

Interesting Fact: Companies investing in employee safety training see 30% fewer claims within three years.

Conclusion: Stop Believing the Myths

Workers’ compensation insurance is not optional. Misconceptions like “only for dangerous jobs” or “too expensive” put businesses and employees at risk. Knowing what it covers, how premiums work, and how claims operate can save money, prevent legal issues, and protect employees.

Remember: Knowledge is power. Don’t fall for myths, train your workforce, and invest in proper workers’ compensation insurance.

Call to Action

Stop letting myths guide your decisions. Compare workers’ compensation insurance policies today to ensure compliance, protect employees, and secure your business. Affordable coverage is available for companies of all sizes—don’t wait until an accident happens.

InsureDirect.com

Corporate Home Office

618 South Broad Street

Lansdale, Pennsylvania 19446

Email: contact@insuredirect.com

Phone: (800) 807-0762 ext. 602

Keep your home safe and secure with complete protection from InsureDirect—because your home deserves nothing less than the best.