Life insurance? Confusing sometimes, but crucial. Term, whole life, oh my! Some people need temporary coverage, others want protection forever. Choosing wrong can hurt financially.

Term Life Insurance – Quick Coverage

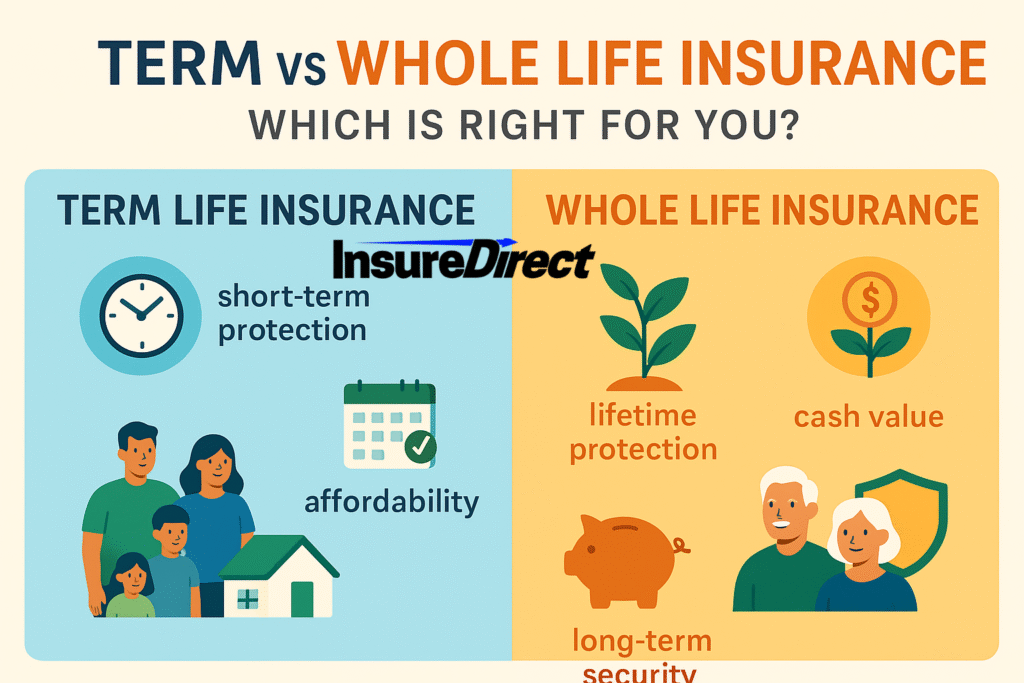

Term life insurance gives protection for a set period—10, 20, or 30 years maybe. If you pass during the term, your beneficiaries get a payout. If not? Nothing happens.

-

Cheap, especially if you’re young.

-

Duration fixed; ends eventually.

-

Death benefit only, no savings or cash value.

Example: You’re 30, buy a 20-year term. Mortgage safe, kids covered. After 20 years, reevaluate or pay more.

Whole Life Insurance – Lifelong Security

Whole life insurance lasts for your whole life, as long as premiums are paid. Cash value grows slowly, premiums mostly fixed. But expensive—often much higher than term.

-

Lifetime coverage, no expiration.

-

Cash value accumulation, like a forced savings account.

-

Predictable premiums.

-

Costly; requires budget planning.

Example: Buy at 30. Covered forever. Cash value exists. Growth slow, but security guaranteed.

Term vs Whole Life – Main Differences

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage Duration | Fixed (10–30 years) | Lifetime, no expiration |

| Premiums | Lower, affordable | Higher, consistent |

| Cash Value | None | Accumulates over time |

| Flexibility | Sometimes convertible | Limited flexibility |

| Ideal For | Short-term obligations | Long-term security & investment |

Pros & Cons of Term Life

Pros:

-

Affordable for young adults or families.

-

Easy to understand, no complexity.

-

Matches temporary obligations like mortgages or tuition.

Cons:

-

Ends eventually; renewal costs often high.

-

No cash value; cannot borrow or save.

-

Premiums increase if renewed after term expires.

Pros & Cons of Whole Life

Pros:

-

Lifetime coverage ensures protection for life.

-

Cash value grows slowly; usable for emergencies or savings.

-

Premiums stable over time.

Cons:

-

High cost.

-

More complex than term; fine print matters.

-

Cash value grows slowly compared to other investments.

Who Should Choose Term Life?

Best for:

-

Parents with children.

-

Homeowners with mortgages.

-

People needing affordable short-term coverage.

Keywords: affordable term life insurance, term life benefits, best term life policies

Who Should Choose Whole Life?

Best for:

-

People seeking lifelong coverage.

-

Those interested in cash value accumulation.

-

Able to afford higher premiums comfortably.

Keywords: whole life insurance advantages, permanent life insurance, life insurance with cash value

Factors to Consider

Before choosing term vs whole life:

-

Budget: cheap now vs expensive now but lifetime coverage.

-

Financial goals: temporary protection or lifelong security?

-

Dependents: who relies on your policy?

-

Investment potential: cash value grows slowly.

-

Age & health: young and healthy = lower premiums.

Combining Term and Whole Life

Hybrid approach works. Term for temporary coverage, whole life for lifelong protection. Cost-effective, balanced.

Example: 30-year-old buys 20-year term for mortgage + small whole life for lifetime security. Coverage balanced.

Keywords: hybrid life insurance, combination policies, term + whole life

Conclusion

Term or whole life? Depends on goals:

-

Term life: affordable, short-term needs.

-

Whole life: lifelong coverage, cash value, legacy planning.

-

Hybrid: best of both worlds.

Choose carefully; family’s financial security depends on it.

Contact InsureDirect

InsureDirect.com

Corporate Home Office

618 South Broad Street

Lansdale, Pennsylvania 19446

Email: contact@insuredirect.com

Phone: (800) 807-0762 ext. 602

Keep your home safe and secure with complete protection from InsureDirect—because your home deserves nothing less than the best.